Capital Gains vs. Business Income: Tax Impacts for Flippers

Flipping properties can be profitable, but taxes can significantly impact your earnings. The IRS may classify your profits as either capital gains or business income, and the difference in tax rates is huge:

- Capital Gains Tax: Long-term rates range from 0% to 20%, depending on income.

- Business Income Tax: Ordinary rates go up to 37%, plus 15.3% self-employment tax.

Key Factors That Determine Your Tax Classification:

- Capital Gains: Profits qualify if properties are held for over 1 year, used as investments, and involve minimal improvements or sales activity.

- Business Income: Frequent flips, short holding periods, and major renovations are taxed as business income.

Quick Comparison:

| Aspect | Capital Gains | Business Income |

|---|---|---|

| Tax Rate | 0–20% (long-term) | Up to 37% + 15.3% SE tax |

| Holding Period | Over 1 year (long-term) | Short-term or frequent flips |

| Deductions | Limited to sale expenses | Broad range of business expenses |

| Additional Taxes | None | Self-employment tax applies |

Pro Tip: Holding properties for over a year often results in lower taxes. For frequent flippers, detailed records and tax planning are critical to maximizing deductions and minimizing IRS scrutiny.

Read on to learn how to classify your activities, reduce tax burdens, and keep more of your profits.

Capital Gains Tax Basics

What Are Capital Gains

Capital gains refer to the profit you make when selling a property for more than you paid for it. These gains are subject to taxation, which directly affects your overall profit.

The IRS divides capital gains into two categories based on how long the property was held:

| Holding Period | Tax Classification | Tax Rate |

|---|---|---|

| 1 year or less | Short-term capital gains | Taxed as ordinary income (up to 37%) |

| More than 1 year | Long-term capital gains | 0% to 20%, depending on income level |

Long-term capital gains are taxed at lower rates compared to ordinary income. For high-income earners, the maximum rate is 20%, which is much lower than the top rate for short-term gains. This makes holding property for over a year an attractive option for reducing tax costs. Now, let’s look at how profits qualify as capital gains.

When Profits Count as Capital Gains

Not all property sale profits automatically qualify as capital gains. The IRS uses specific criteria to determine whether your profits are taxed as capital gains or as business income:

- Primary Purpose: The property must be purchased as an investment, not for immediate resale.

- Holding Period: To qualify for long-term rates, you need to hold the property for more than one year.

- Business Activity: Minimal advertising aligns more with capital gains treatment.

- Improvement Scope: Renovations should be modest and focused on maintenance rather than flipping.

"Many investors fail to plan for the tax consequences of flipping real estate and end up sharing too much profit with an uninvited partner: the IRS." - Socotra Capital

To qualify as an investor (and benefit from capital gains tax treatment), you need to show that you:

- Hold properties primarily for appreciation.

- Make limited improvements aimed at basic upkeep.

- Conduct a small number of transactions annually.

- Often generate rental income while holding the property.

If the IRS classifies you as a dealer-trader instead of an investor, you won’t qualify for long-term capital gains rates, no matter how long you hold the property. Understanding the difference between investor and dealer status is essential for effective tax planning.

Business Income Tax Rules

What Is Business Income

When the IRS views property flipping as a business activity, profits are treated as regular business income instead of capital gains. This classification means the income is taxed at ordinary income tax rates, which are generally higher than the rates for long-term capital gains.

Dealer flippers are subject to federal income tax rates ranging from 10% to 37%, a 15.3% self-employment tax (split into 12.4% for Social Security and 2.9% for Medicare), and applicable state taxes. For instance, a dealer earning $200,000 annually might face around $71,411 in federal taxes - split into about $40,811 for income tax and $30,600 for self-employment tax - resulting in an effective tax rate of 35.71% [4].

How the IRS Decides

The IRS uses specific factors to determine whether flipping activities qualify as a business rather than an investment. Here's what they look for:

| Factor | Indicators of Business Activity (Dealer) |

|---|---|

| Transaction Frequency | Regular and frequent buying and selling |

| Property Purpose | Purchased with the intent to resell |

| Marketing Efforts | Active advertising or promotional activities |

| Improvements | Major renovations aimed at increasing profit |

| Holding Period | Short-term ownership before resale |

| Income Source | A primary or substantial source of income |

If your activities meet these criteria and are classified under dealer status, several tax rules come into play:

- Properties are treated as inventory, not capital assets.

- You won't qualify for long-term capital gains tax rates.

- 1031 exchanges for deferring taxes are not allowed.

- Profits must be reported on Schedule C.

- Quarterly estimated tax payments are required.

This classification also impacts deductions. Dealers can claim a variety of expenses, including:

- Property improvement costs for sold properties

- Interest on real estate loans

- Property taxes

- Building permit fees

- Office supplies and expenses

- Legal and accounting fees

- Travel costs related to the business

- Sales commissions

- Home office expenses (based on the space used for work)

To make the most of these deductions and avoid IRS issues, keep detailed records and maintain separate accounts for each property. Proper documentation is key to ensuring compliance and maximizing your tax benefits.

Tax Differences Between Capital Gains and Business Income

Tax Rates and Write-offs

The tax treatment for property flippers differs significantly depending on whether profits are classified as capital gains or business income. Here's a breakdown:

| Aspect | Capital Gains | Business Income |

|---|---|---|

| Tax Rate | 0–20% (long-term) | Up to 37% plus 15.3% self-employment tax |

| Additional Taxes | None | Self-employment tax |

| Deductions | Limited to cost basis and sale expenses | Broad range of business expenses |

| QBI Deduction | Not eligible | Up to 20% of qualified income |

For example, a $200,000 profit treated as business income would result in around $71,411 in federal taxes. This includes $40,811 in income tax and $30,600 in self-employment tax, leading to an effective tax rate of 35.71%. Now, let’s look at how losses are handled under each classification.

Handling Losses

Losses are treated differently based on the classification:

-

Business Income Losses: These can be fully deducted in the year they occur. Tax expert Paul Allen from PIMTAX explains:

"Whatever you lose on the house in the year of the sale can be completely deducted from your taxes in that year" [1].

- Capital Losses: These are capped at a $3,000 annual deduction against ordinary income. Any excess losses must be carried forward to future years and can only offset other capital gains beyond the $3,000 limit [1].

Finally, let's explore how home sale tax benefits apply under capital gains rules.

Home Sale Tax Break

The primary residence exclusion is a major benefit under capital gains rules. It allows exclusions of up to $250,000 for single filers or $500,000 for married couples. However, this benefit doesn’t apply to business income [6]. Property flippers classified as dealers are disqualified from using this exclusion.

For flippers aiming to reduce their tax burden, keeping detailed records of all expenses is critical. Consulting with tax professionals can help determine the best approach, especially since the broad range of deductions available under business income can offset higher tax rates for those with substantial operating expenses [7].

Related video from YouTube

sbb-itb-16b8a48

Anti-Flipping Tax Rules

The IRS has specific rules to prevent investors from taking unfair tax advantages through quick property sales. These guidelines determine whether profits are taxed as capital gains or as regular business income. Here's a breakdown of the key rule and its exceptions.

1-Year Property Hold Rule

If you sell a property within 12 months of buying it, the IRS takes a closer look. Profits from these sales are taxed as ordinary income, which can go as high as 37%, plus an additional 15.3% self-employment tax. On the other hand, holding a property for more than a year usually qualifies you for long-term capital gains tax rates, which are significantly lower - ranging from 0% to 20% - and avoid the self-employment tax.

| Holding Period | Tax Classification | Tax Rate | Additional Taxes |

|---|---|---|---|

| Under 1 Year | Business Income/Short-term Gains | Up to 37% | 15.3% Self-employment Tax |

| Over 1 Year | Long-term Capital Gains | 0–20% | None |

This difference makes the holding period a key factor in tax planning, especially when exceptions to the rule come into play.

Exceptions to the Rule

In certain cases, a quick property sale may still qualify for capital gains treatment. Examples of qualifying life events include serious illness, major changes in household, job relocations, or issues with the property beyond your control [8][9].

The IRS reviews these situations on a case-by-case basis. They consider factors like how often you sell properties, any improvements made, marketing efforts, and whether your activities resemble a business [4]. To claim an exception, you need to show that the sale was due to these qualifying circumstances and not part of regular flipping activities.

Keeping detailed records of these events is crucial to support your case if the IRS questions your tax classification [9].

Tax Planning for Flippers

Effective tax planning can make a big difference in your flipping profits. By organizing your activities and keeping thorough documentation, you can reduce tax liabilities and keep more of your earnings.

Record Keeping

Accurate record-keeping is essential. Use a separate checking account for each property to avoid mixing expenses. Track all property-related transactions carefully, including:

| Expense Category | Examples | Tax Impact |

|---|---|---|

| Capital Expenditures | Renovation costs, Building materials | Lowers taxable profit |

| Operating Costs | Property taxes, Insurance, Utilities | Deductible as business expenses |

| Professional Fees | Legal services, Accounting fees | Direct write-off |

| Marketing Expenses | Real estate commissions, Advertising | Deductible as business expenses |

"Seeking expert tax advice up front will help ensure maximum tax benefits and minimum payouts for your business." - Socotra Capital [3]

Next, consider how the timing of your sales can further improve your tax strategy.

Sale Timing

When you sell a property can have a big impact on your taxes. Holding a property for over 12 months may qualify it for long-term capital gains tax rates, which are often lower. Here are some timing strategies to keep in mind:

- Loss Harvesting: Offset gains by selling other properties at a loss within the same tax year [3].

- Rental Conversion: Temporarily convert a flip property into a rental to strengthen your investor classification [5].

- Primary Residence Strategy: Live in a flip property as your primary residence for at least two years to potentially benefit from residential tax breaks [5].

Working with Tax Experts

Tax laws can be complicated, but working with a professional can simplify things. Tax experts can help you navigate the rules and maximize your savings. As Tim Yoder, Ph.D., CPA, explains, treating flips as assets instead of inventory can lead to substantial tax savings [5].

Here’s how tax professionals can assist:

- Choose the best business structure, like an LLC or S-corporation.

- Identify all possible deductions.

- Plan transactions to reduce tax obligations.

- Ensure compliance with IRS requirements.

- Strategize the timing of property purchases and sales.

For those flipping properties regularly, setting up an S-corporation can help lower self-employment taxes while keeping the benefits of flow-through taxation [5]. However, this requires careful planning and guidance from an experienced professional.

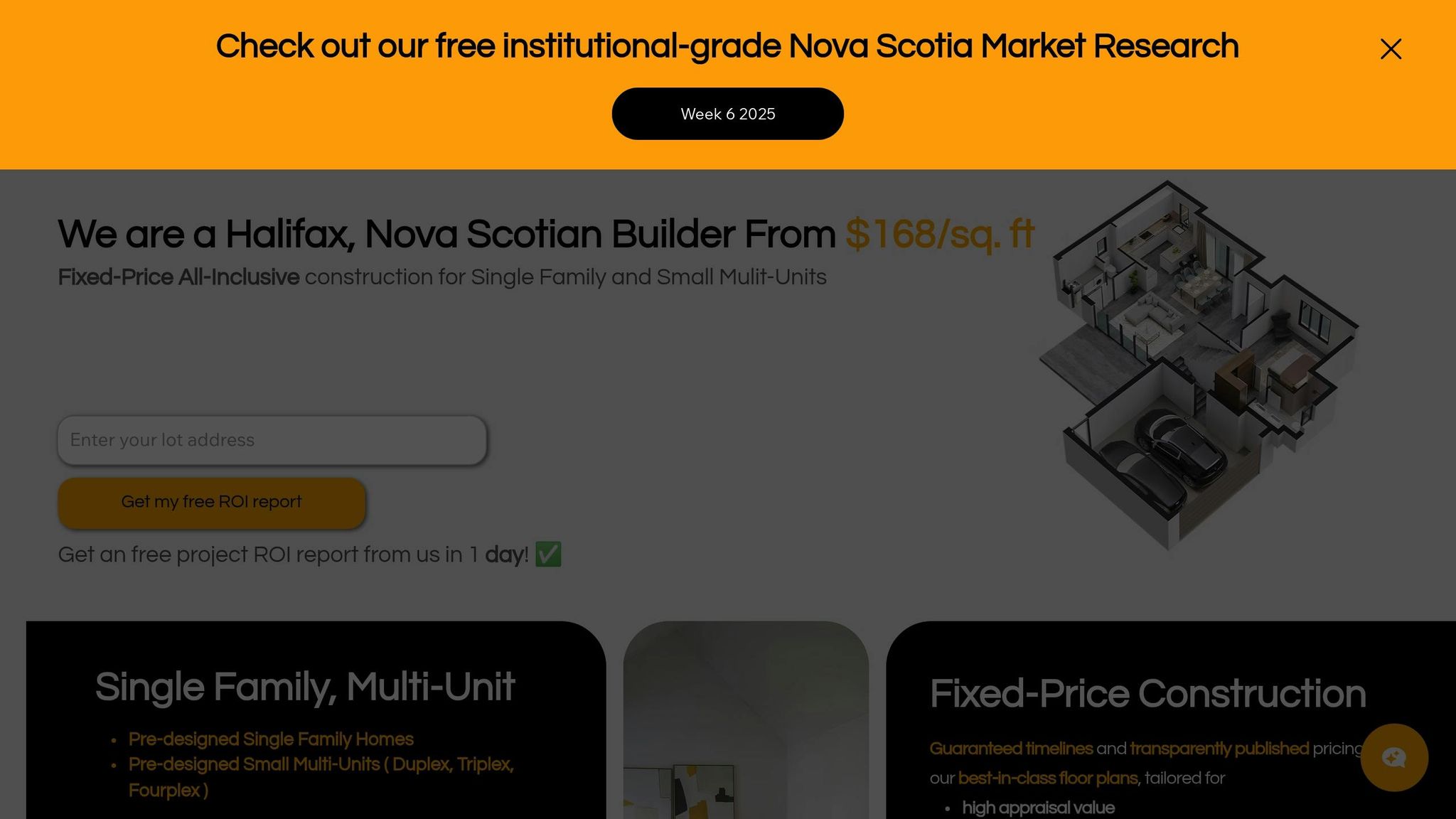

Helio Urban Development Services

Helio Urban Development offers a fixed-price model that helps property flippers manage costs effectively and plan taxes with ease. This approach simplifies challenges related to tax planning by focusing on new construction, aligning with the need for clear and predictable cost management.

About Helio Urban Development

Helio Urban Development focuses on building new properties for investors in Nova Scotia, with prices starting at $168 per square foot for single-family homes. Their services allow investors to compare the tax effects of new construction versus renovation projects.

Here’s a breakdown of their pricing:

| Property Type | Starting Price |

|---|---|

| Single-Family | $168/sq.ft |

| Duplex Units | $175/sq.ft |

| Multi-Unit (4-8) | Custom |

This pricing model supports straightforward depreciation schedules and avoids the hassle of separating repairs from capital improvements[12].

Key advantages for investors focused on taxes include:

- Clear cost documentation that simplifies calculating a property's cost basis for depreciation[11].

- New construction that eliminates the need to classify expenses as repairs or capital improvements[12].

- Investor-friendly designs tailored for business entities like LLCs or S-corporations, making it easier to deduct business expenses[2][10].

Conclusion

Navigating property flip taxes effectively can help you maximize profits while staying compliant with IRS regulations. The way your income is classified - either as capital gains or business income - plays a major role in determining your tax liability. For instance, dealer profits can face combined taxes as high as 35.71% [4], whereas investors holding properties for over a year may only pay 0–20% on long-term gains [4]. This underscores the importance of careful tax planning.

To manage taxes more efficiently, consider forming an LLC or S Corporation. These structures can safeguard your assets and open up additional deduction opportunities [4]. Be diligent about tracking expenses, such as the $0.67 per mile standard rate for 2024 [3], and work with a real estate tax expert to fine-tune your approach.

Here’s a quick comparison of the tax implications for dealers versus investors:

| Tax Category | Dealers (Flippers) | Investors |

|---|---|---|

| Tax Rate | Ordinary Income (up to 37%) + Self-Employment (15.3%) | Long-term Capital Gains (0–20%) |

| Available Benefits | Business Expense Deductions | 1031 Exchange, Depreciation, 121 Exclusion |

| Holding Period Impact | Limited Tax Benefits | Significant Tax Advantages |

Donald P. Gould of Gould Asset Management explains the advantage of long-term gains perfectly:

"The most important thing to understand is that long-term realized capital gains are subject to a substantially lower tax rate than ordinary income. This means that investors have a big incentive to hold appreciated assets for at least a year and a day, qualifying them as long-term and for the preferential rate" [14].

It’s also worth noting that rolling proceeds into another project doesn’t defer taxes for dealer activities [13]. As discussed earlier, a solid tax strategy combined with detailed record-keeping is key to success in property flipping.