Guide to CMHC-Insured Loans for Multi-Unit Properties

CMHC-insured loans are a powerful tool for developers and investors in Canada, offering better financing terms for multi-unit residential projects like apartments, student housing, and retirement homes. These loans reduce lender risk, resulting in lower interest rates, higher borrowing limits, and longer repayment periods. Here's a quick breakdown:

- Interest Rates: 1–1.5% lower than conventional loans.

- Loan-to-Value (LTV): Up to 85% for most properties; up to 95% for qualifying projects.

- Down Payment: As low as 15% (compared to 25–35% for standard loans).

- Amortization Period: Up to 40–55 years, depending on the program.

Key Benefits:

- Lower Costs: Reduced interest rates and insurance premiums.

- Extended Terms: Longer repayment periods mean lower monthly payments.

- Higher Borrowing Limits: More financing options for multi-unit developments.

CMHC-insured loans support various property types, including standard rentals, supportive housing, and student housing, with specific requirements like a minimum of 5 units and compliance with accessibility and energy efficiency standards. Programs like MLI Select offer additional incentives for affordability, energy efficiency, and accessibility.

For developers and investors, these loans make multi-unit projects more financially viable while addressing Canada’s housing shortage.

Is CMHC's MLI Select Mortgage Good For Multi-Unit Investment Properties?

Who Can Apply

CMHC-insured loans are available for eligible multi-unit residential properties and qualified borrowers.

Approved Property Types

CMHC insurance supports various multi-unit residential properties, each with specific requirements. A key condition is that properties must include at least 5 residential units [3].

| Property Type | Key Requirements | Special Considerations |

|---|---|---|

| Standard Rental Housing | Minimum 5 units | Non-residential space limited to 30% |

| Student Housing | Purpose-built complexes | Must be located near educational institutions |

| Retirement Homes | Minimum 50 units/beds | Includes facilities offering specialized care |

| Supportive Housing | 5+ units | Must provide support services |

| Single Room Occupancy | 5+ units | Shared facilities are acceptable |

For properties with commercial space, specific limits apply. The commercial area cannot exceed 30% of the gross floor area or 30% of the total lending value [4].

Property Standards

In addition to meeting property type requirements, properties must adhere to strict standards:

- Location: Properties must be in Canada and free from restrictions on non-Canadian purchases.

- Occupancy: They must be suitable for year-round living.

Accessibility is another major consideration. CMHC uses a point-based system to evaluate accessibility features:

"All units in the building (i.e., both accessible and non-accessible units) must be 100% visitable in accordance with Canadian Standards Association (CSA) standard B651:23 and common areas are barrier-free in accordance with B651:23." [4]

The CMHC MLI Select program evaluates properties on three main criteria:

- Affordability: Units priced at 30% of the median renter income.

- Energy Efficiency: Demonstrated reductions in energy use compared to current performance.

- Accessibility: Compliance with CSA B651:23 and Rick Hansen Foundation Accessibility Certification Version 4.0 standards.

Properties that achieve qualifying scores across all categories can benefit from reduced premiums and longer amortization periods. These features are key to securing the favorable rates and flexible terms mentioned earlier [4].

Main Advantages

CMHC-insured loans offer several benefits that make housing projects more financially viable. These include reduced costs, extended repayment terms, and increased borrowing limits.

Lower Costs and Better Rates

One major perk of CMHC-insured loans is access to preferred interest rates and reduced insurance premiums. Programs like MLI Select provide specific incentives that significantly lower borrowing expenses, which can be a game-changer for developers.

"While ACLP provides much-needed funding that makes development possible, MLI Select offers mortgage loan insurance with better financing terms for the project... In simple terms, ACLP helps projects get the green light, and MLI Select helps ensure projects remain financially viable over time through insurance incentives. By leveraging both programs, developers can benefit from comprehensive support throughout the lifecycle of a rental housing project, from construction to long-term financing." [2]

Extended Payment Terms

CMHC-insured loans also come with longer repayment periods, providing added flexibility. For new construction market projects, amortization periods can now stretch up to 50 years. Loans under the MU MLI program also offer 50-year terms, while MLI Select projects may qualify for up to 55 years [5]. These extended terms lower monthly payments and improve affordability. For example, a borrower with an annual income of US$100,000 can now afford monthly payments of up to US$3,250, increasing their maximum mortgage eligibility from US$616,000 to US$687,000 [7].

Higher Borrowing Limits

Another advantage is the ability to borrow more. The MLI Select program allows up to 95% loan-to-value (LTV) for new construction projects that meet minimum scoring requirements. Existing properties can achieve LTV ratios between 85% and 95%, depending on their scores. Retirement homes with 50 or more units also qualify for favorable LTV terms.

"These programs help multi-unit projects pencil out. However, they do not address the other pressures experienced by developers in the past year, including volatility in construction costs, the high cost of land for development sites, municipal fees and development charges, and increased operating costs." [2]

sbb-itb-16b8a48

How to Apply

To successfully secure a CMHC-insured loan for multi-unit properties, it's important to follow a clear process and ensure all details are in order. Here's how to navigate the application process effectively.

Application Steps

Applying for a CMHC loan involves several key stages. It's wise to work with a mortgage broker who has experience with these loans. Here's what to expect:

-

Pre-Application Assessment

Start by getting pre-approved. This helps determine how much you can borrow. Sit down with your financial advisor to confirm your eligibility and assess your financial readiness. -

Document Preparation

Gather and organize all necessary documents. Your application should clearly show that you're financially capable and that your project is feasible. -

Submission and Review

Submit your completed application through an approved lender. During the review, both your income and the viability of the property will be evaluated.

Make sure your documentation is thorough and well-prepared to support your application.

Required Documents

Your application package needs to include detailed documentation across several areas. Here's what you'll need:

| Category | Required Documentation |

|---|---|

| Financial Records | • Income statements (last 2 years) • Balance sheets • Cash flow projections • Verification of funding sources |

| Property Documentation | • Property appraisal • Zoning compliance certificates • Lease agreements (if applicable) • Title documentation |

| Project Planning | • Detailed construction timeline • Environmental assessments • Energy efficiency reports • Market analysis |

| Legal Documents | • Corporate structure details • Proof of property ownership • Compliance certificates |

Having all these documents ready will help streamline the process.

Processing Time

For standard applications, you can expect an initial response within 2–5 business days [8]. However, the total processing time can vary based on factors like how complete your application is, the complexity of the property, and how quickly you respond to requests. For more complex projects, the process might take several months [9].

Costs and Financial Analysis

Understanding the costs of CMHC-insured loans is crucial for anyone involved in multi-unit investments. Let’s break down how premium rates work, compare these loans with conventional financing, and see how they impact overall project costs.

Premium Rates

CMHC insurance premiums are calculated based on factors that assess the loan's risk. These premiums are non-refundable and usually added to the mortgage amount [10]. Key charges include:

- 0.25% surcharge for every additional 5 years beyond a 25-year base.

- 1% fee for non-residential areas.

- 0.50% charge on any outstanding second mortgage balances.

For construction projects, premiums are paid as funds are disbursed [10]. The MLI Select program offers a more cost-effective option, especially for projects with higher leverage and longer amortization periods [6].

CMHC vs. Standard Loans

CMHC-insured loans stand apart from conventional commercial loans in several ways:

- Interest Rates: CMHC loans typically come with lower rates due to the insurance backing.

- Maximum Financing: You can finance up to 85% of a property's value, compared to 65–75% with conventional loans.

- Down Payment: CMHC loans allow down payments as low as 15%, while conventional loans often require 25–35%.

- Amortization Period: CMHC loans can stretch up to 40 years, compared to the standard 25–30 years for traditional loans.

- Property Eligibility: These loans are designed for multi-unit residential properties, whereas conventional loans might cover a broader range of commercial properties.

These terms can improve cash flow and lower upfront costs [1].

Total Cost Impact

While CMHC insurance adds an upfront premium, the long-term benefits can outweigh this initial expense. Lower interest rates and extended amortization periods result in savings over time.

The MLI Select program offers even more financial perks:

- Lower Capital Requirements: Down payments can be as low as 5%, freeing up funds for other needs [11].

- Extended Amortization: Terms of up to 50 years can reduce monthly payments, improving cash flow [11].

- Interest Savings: Reduced rates can lead to significant savings over the life of the loan [10].

Example Projects

Success Stories

CMHC-insured loans have played a key role in several multi-unit developments across Canada. Here are two standout examples:

An Ontario real estate developer partnered with Sunlite Mortgage to use the MLI Select program. Initially, a buyer qualified for just two units under traditional financing. But with MLI Select's 95% loan-to-value (LTV) option, the buyer expanded their purchase to five units. This not only helped the developer sell units faster but also cut down on carrying and interest costs, boosting overall returns [12].

Another example involves an investor who acquired a $2.5 million multi-unit building with just a $125,000 down payment (5%). The property generated $13,800 in monthly rent, resulting in a $5,000 monthly net cash flow. Within a year, the building's value grew by 10%, reaching $2.75 million and adding $250,000 in equity. By refinancing through MLI Select, the investor tapped into this equity to purchase another property [12].

These examples showcase how CMHC-insured financing can be tailored to meet diverse investment goals, with support from regional experts like Helio Urban Development.

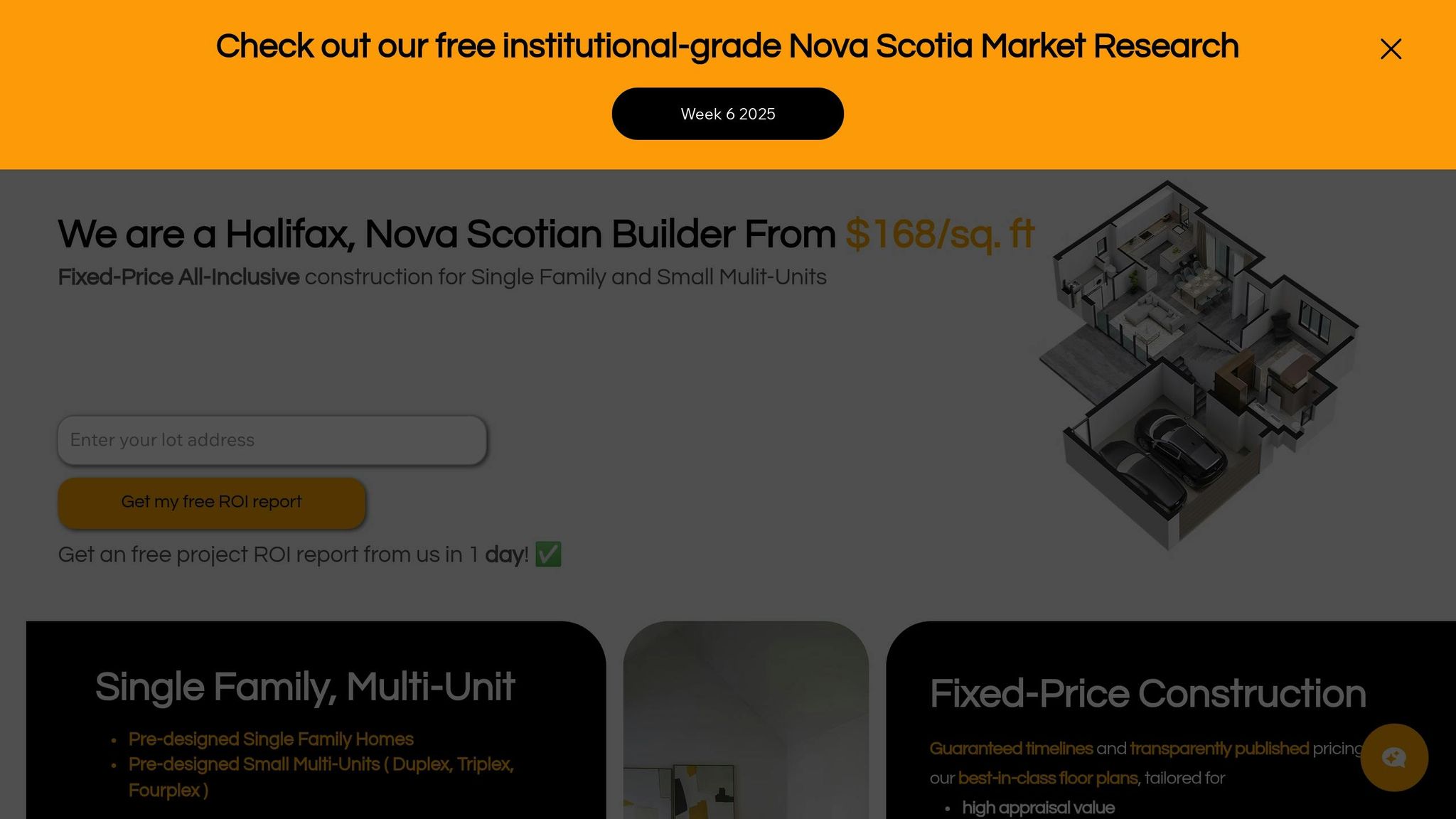

Helio Urban Development Services

In Nova Scotia, Helio Urban Development specializes in fixed-price construction for small multi-unit projects, designed to align with CMHC-insured financing. With costs starting at $168 per square foot, their approach provides investors with clear and predictable budgets - an essential factor for CMHC loan applications.

| Aspect | Benefit |

|---|---|

| Cost Efficiency | Predictable expenses for better planning |

| Project Timeline | Pre-designed plans speed up approvals |

| Investment Returns | Smart layouts boost rental income potential |

This approach is backed by CMHC's broader efforts. As of September 2024, CMHC has committed $20.65 billion in loans through the ACLP program, enabling the creation of over 53,000 purpose-built rental homes [2].

These case studies emphasize how CMHC-insured loans make multi-unit development more efficient and scalable.

Summary and Future

Main Points

CMHC-insured loans offer multi-unit developers and investors a way to cut costs and gain more financial flexibility. These loans feature interest rates that are 1–1.5% lower than conventional loans, loan-to-value ratios of up to 85%, and amortization periods extending up to 40 years, making projects more feasible [1].

With these benefits in place, recent policy updates suggest key adjustments that will shape future projects.

Future Changes

By Q3 2024, CMHC had insured nearly 65,000 multi-unit residential units - up 26% from 2023 [14]. Recent updates include a shift to a risk-based approach for construction loan leverage, stricter requirements for lease-up periods, and mandatory appraisals for all insured properties, all of which will influence future loan terms [13].

CMHC estimates Canada’s housing stock will grow by 2.3 million units by 2030, but an additional 3.5 million homes will still be needed to meet affordability goals [2]. Purpose-built rental construction is on the rise, accounting for 47% of housing starts in Canada’s six largest metropolitan areas in 2024 [2].

As CMHC’s framework evolves, developers will face increased scrutiny regarding market risks, project details, and their own experience. New measures also stress accessibility standards and environmentally conscious planning, requiring these elements to be integrated early in the project timeline [13].

"These measures collectively help make rental housing projects more viable and attractive, ultimately contributing to an increased supply of affordable and sustainable rental housing in Canada... The CMHC's financing programs, while impactful, are a single factor in the development pro forma."

– Kerri Byers, Associate Director, Valuation Advisory at Altus Group [2]

These updates highlight CMHC’s focus on supporting multi-unit development while balancing risk management and long-term project success.